ChainThink

Stay ahead, master crypto insights

From Application Process to Fees: A Deep Comparison of the Top Ten Cryptocurrency Payment Cards

From Application Process to Fees: A Deep Comparison of the Top Ten Cryptocurrency Payment Cards

2025-04-19 14:21

Author: jk, Odaily Star Daily

As the global cryptocurrency infrastructure gradually matures, the demand for "real-world usability" of on-chain assets is growing. However, how to truly use on-chain assets in real life has always been a concern for crypto users.

Cryptocurrency payment cards (also known as "U Cards") have quietly emerged against this backdrop - they not only bridge the "last mile" of asset usage, but are also quietly reshaping people's understanding of wallets, PayFi, and payment networks.

Whether it is directly binding mobile payment software for consumption, or mortgaging Bitcoin to borrow stablecoins to flexibly cope with market conditions, the ways of using cryptocurrency payment cards are becoming more diverse. Among them, some are based on exchanges, focusing on stability and cashback rewards, while others are based on wallets or protocols, emphasizing on-chain native assets and composability. Today's cryptocurrency payment cards have become a practical and increasingly mature entry point into the crypto finance world.

To clarify the real user experience and differences of these products, Odaily Star Daily conducted an in-depth analysis of the ten most representative cryptocurrency payment cards in the current market based on extensive information collection and user feedback on social platforms, including Bybit, Bitget, SafePal, Morph, Infini, Coinbase, Nexo, MetaMask, 1inch, and RedotPay, systematically sorting out and comparing their application thresholds, supported assets, fee structures, cashback mechanisms, and on-chain interaction capabilities, helping readers find the best "pass" in this rapidly evolving field.

New U Cards for Chinese Users

Bybit Card: The Most Widely Used Exchange U Card

Bybit's newly launched virtual debit card has become popular on social media recently due to its no annual fee and low threshold. This card supports KYC certification in mainland China, and the application process is free.

The application process is quite simple: first, users need to register a Bybit account, and after registration, complete identity verification on the platform. It is reported that users with Chinese identities can pass KYC verification. After passing the verification, go to the homepage and find the "Card" option to enter the application page, then users can choose different regions to open a card:

-

Choose Australia as the card opening region. If this option is selected, applying for a virtual card does not require providing address proof. After submitting the application, the review time is approximately 5 to 7 working days. In this version, the default currency of the card is USD.

-

Users can also choose the European Economic Area (EEA), but it should be noted that the EEA version requires providing address proof of the European Economic Area, such as utility bills or credit card statements from Europe. In this version, the default currency of the card is EUR.

In terms of usage, this card can be managed within the Bybit App. The virtual card can be directly bound to Apple Pay, Google Pay, etc., for consumption, and can be used at any merchant that supports Mastercard globally.

Recent Twitter messages indicate that the Australian version of the virtual card can no longer bind Alipay and WeChat Pay for consumption, which is mainly due to excessive utilization by "suckers' studios". However, some users have reported that Alipay's "touch to pay" can be used for transactions, which may vary depending on each user's account risk control. If you need to bind these payment tools, you can consider applying for the European card version. According to Twitter information, the European card version is still able to bind Alipay and other tools for use at present.

Regarding fees, Bybit card has considerable competitiveness: transaction fees range between 0.9% to 3%, depending on the card issuing region, transaction currency, and location of consumption. Some transactions may incur additional intermediary fees (such as Alipay). The platform is currently running a new card promotion, and users can enjoy a 10% cashback discount on their spending.

It should be particularly noted that different regions may incur additional costs such as currency conversion fees. For example, if a user swipes the card at a merchant that uses Japanese Yen, the final fee may include the exchange rate from USD/EUR to Japanese Yen, and this part must be borne by the user. Overall, this card has obvious advantages in terms of usage due to its connection with the exchange, making it one of the more convenient choices in the current market.

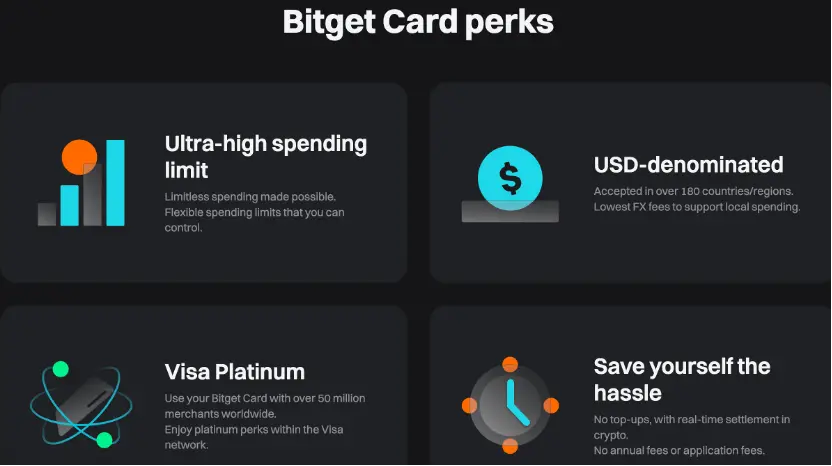

Bitget Card: Exclusive Payment Card for VIPs

Compared to traditional bank cards, Bitget's virtual debit card also offers "no annual fee" and "direct consumption of USDT" as main selling points, attracting the attention of many crypto users. This card currently supports two card organization options: UnionPay and Mastercard, covering the actual needs of different regions and consumption scenarios.

The issuer of the Bitget card is the DeCard brand, a regulated issuing bank in Singapore, according to market reports, has been acquired by Bitget majority equity. Although DeCard also provides card application services for individual users, this path usually requires applicants to have local identity authentication and phone numbers in Singapore, with higher thresholds. Therefore, applying through the Bitget platform is a more feasible way.

It should be noted that the Bitget card is not currently open to all users. According to the platform's current rules, only users who reach the VIP level are eligible to apply, and one common threshold is that the account balance needs to reach 30,000 USDT or equivalent assets. Therefore, the target user group of this card is more focused on high-net-worth or active trading users.

Currently, the Bitget card also supports binding operations for Apple Pay, Google Pay, Alipay, and WeChat Pay, focusing on the liquidity release of on-chain assets and daily consumption. It should be noted that there are different types of Bitget cards. The Bitget card on the official website is a Visa card with USD as the underlying settlement currency, while the popular Bitget Premium Payment Card on Twitter is a Mastercard/UnionPay card with Singapore dollars as the underlying settlement currency, which is slightly different. According to user experiences on Twitter, this card can be smoothly used anywhere that supports Mastercard.

At the same time, Bitget states on its homepage that there will be BGB cashback opportunities in the future.

At the same time, Bitget states on its homepage that there will be BGB cashback opportunities in the future.

From the perspective of fees, the transaction fee of the Bitget card is also 0.9% to 3% , mainly affected by the transaction currency, consumption location, and whether currency exchange is involved. For example, if a transaction is settled in USDT in a region other than USD/Singapore dollar, it may trigger certain currency exchange fees. In addition, different payment channels (such as UnionPay and Mastercard) may affect the arrival time and intermediary fees. Also, Alipay and WeChat Pay will charge fees on transactions over 300 yuan.

Overall, the Bitget card, as a virtual financial product derived from the exchange, provides users with another channel to use crypto assets in real-life scenarios, especially suitable for users with large asset sizes and frequent cross-border consumption.

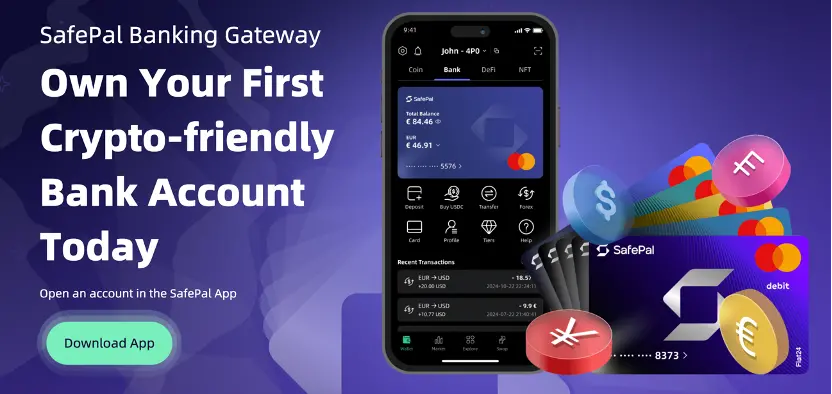

SafePal x Fiat 24: Not Just a U Card, But a Compliant Bank Account

Different from the traditional concept of a "virtual card", SafePal provides a more integrated cryptocurrency financial service, with the underlying account support provided by the Swiss registered bank Fiat 24. After completing identity authentication and address verification, users will receive a real European bank account (with IBAN), which can be used for international deposits, withdrawals, and even for consumption with the associated debit card.

The application process is relatively complex compared to other cards. Users need to first enter the relevant module within the SafePal wallet interface, provided that the account's region supports this service (currently including mainland China). Next, users need to transfer a small amount of ETH on the Arbitrum network to mint an identity NFT, which serves as the necessary token to obtain Fiat 24 banking services. After completing KYC and address verification, the system will assign a Fiat 24 bank account, and users can simultaneously apply for a Mastercard debit card linked to the account. In 2023, some users received Visa cards, and the current mainstream version is Mastercard.

This card also supports binding Apple Pay, Google Pay, Alipay, and WeChat Pay, the underlying settlement currency supports Euros, US Dollars, Swiss Francs, and RMB.

Regarding fees, the comprehensive fee range of the SafePal debit card is 1% to 3%, depending on the specific transaction structure. The withdrawal fee is about 1%, and there is no additional charge for the same currency consumption. For users who have a demand for these four currencies, it is good news. Once the fiat balance on the card is exhausted, the system will automatically deduct from the corresponding crypto balance, enabling the consumption of crypto assets.

At the same time, because users get a complete bank account, this account supports international transfers to major banks, as well as international digital banks like ifast, Wise, Revolut, there are many experiments and fee evaluations on social platforms.

Compared to other exchange-driven card products, SafePal's cooperation with Fiat 24 is closer to the extension of traditional financial services to the crypto world. It provides users not just a card, but a complete financial account that can freely receive and send Euros, link to crypto assets, and has a compliant identity label, especially suitable for users with cross-border income and expenditure needs or asset export needs.

Morph Black Card: The Top of High-End Credit Cards

Morph Black Card is the flagship membership benefit carrier launched by Morph, which focuses on the combination of "on-chain identity + real-world privileges" for high-net-worth crypto users. Unlike traditional virtual debit cards, the application threshold for Morph Black is holding a specific NFT - Morph Black NFT, which currently has a floor price of approximately 0.87 ETH on the secondary market. This NFT not only symbolizes the user's membership status, but also embeds the pricing and circulation function of on-chain financial rights.

In terms of functional design, the Morph Black NFT is officially defined as the flagship asset of the MorphPay ecosystem, and its holders may receive future Morph Token airdrops, enjoying the allocation rights during the lowest fully diluted valuation (FDV) stage. At the same time, the NFT will be linked to multiple ecosystem projects such as BAI Fund to bring airdrop incentives to users, and cardholders can also participate in on-chain deposits on the platform, earning returns with an annualized yield of up to 30%.

Regarding card benefits, the Morph Black Card is a physical black gold card of 22g. After completing KYC, cardholders can apply for this card, the advertised benefits include exemption from the usual $300 annual fee for traditional black cards, and a minimum of 0.3% fee (depending on currency exchange needs) during fund inflow and outflow. This card has a single-day limit of up to $1 million for fund inflow and outflow, and also comes with a Singapore dollar bank account. According to the platform's public information and community discussions, this card will also be integrated with hotel, flight booking, and private concierge services globally, possibly supported by the Aspire VIP system, creating similar travel and lifestyle support services for crypto asset holders as traditional high-end credit cards.

Additionally, according to community and social platform messages, the Morph Black physical card may be built on the DCS (DeCard) issuance system. Its investor Bitget is rumored to have acquired most of DCS's equity, so this card is likely to be developed based on DCS's Mastercard, with some benefits possibly coming from DCS's Black Card Imperium World Elite Card, and it has a credit card mechanism.

According to the Morph team, they will launch a regular card version for a broader user base in the future to expand their payment network and ecological penetration. Overall, the Morph Black Card is one of the most symbolic card products in the current market for "high-end finance," suitable for crypto veterans seeking asset premium and combinable benefits.

It is worth noting that, Morph started selling the Morph Platinum SBT a few days ago. By minting the Morph Platinum SBT, users can ensure their quota rights in the ecosystem under a 500 billion FDV, and unlock 50% of the tokens at TGE. At the same time, SBT holders will receive the Morph Platinum Card (Platinum Card). Details of the card have not been disclosed yet, but it is also a U card that supports direct cryptocurrency consumption, offering a 300-dollar annual black card card benefits trial. Currently, the cost to mint the Morph Platinum SBT is 0.3 ETH.

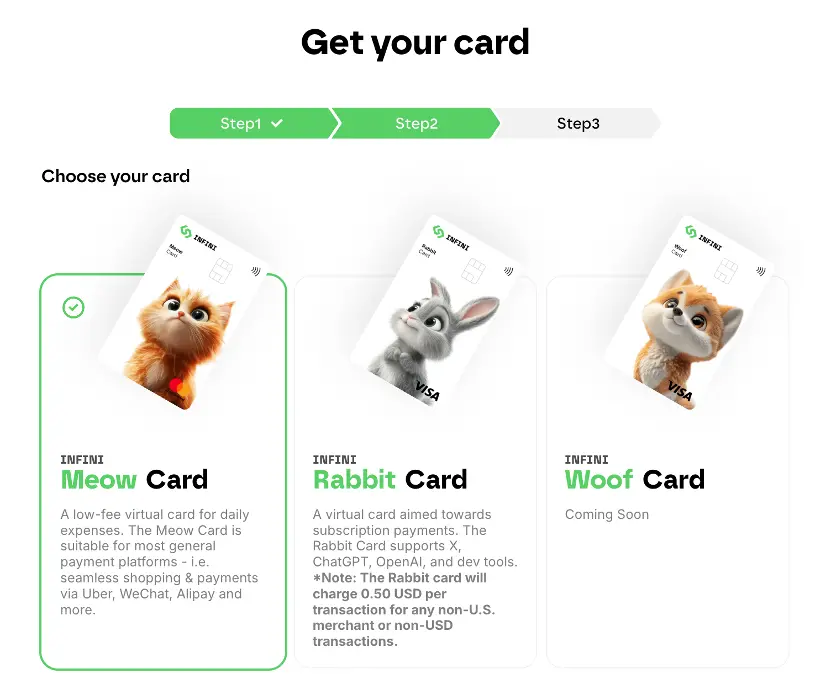

Infini Card: Virtual Card Supporting OnlyFans

Infini has three different types of cards: Meow Card and Rabbit Card are core virtual card products, providing flexible on-chain payment and daily consumption solutions for different user needs. Currently, both cards are sold at a price of $9.9, without annual or monthly fees, and support binding Alipay and WeChat Pay, making it one of the few overseas virtual card products compatible with the mainstream payment tools of Chinese users.

Meow Card belongs to the Mastercard network, more suitable for daily consumption scenarios priced in RMB, its transaction service fee is 0.8% of the transaction amount. When making a non-US Dollar currency payment, the system will automatically perform currency conversion, and charge a 1% to 1.5% cross-border fee, with a minimum of $0.01.

Rabbit Card uses the Visa network, with a focus on USD merchants, especially suitable for a series of subscription-based platforms, including ChatGPT Plus, OpenAI API, Midjourney, Cursor, AWS, Google Cloud, Notion, Godaddy, GitHub, etc., development-related services, as well as mainstream consumer platforms such as Netflix, YouTube, eBay, Amazon, covering almost all the USD subscription services needed in daily life. The basic service fee of Rabbit Card is also 0.8% per transaction, but the fee for non-US merchants or non-US currency transactions is fixed at 1% plus $0.50, with a minimum rate threshold of $0.01.

Certainly, the Infini website also kindly indicates that whether it is Meow Card or Rabbit Card, they both support OnlyFans subscriptions, indeed putting user needs into practice.

Although these two cards are virtual in form, they can be quickly bound to Alipay and WeChat Pay in actual use, achieving a seamless payment experience. On the official website, it can be seen that Infini's physical card product Woof Card is being prepared, and in the future, it will support Apple Pay and Google Pay, and have broader offline payment capabilities, expected to further expand the user base.

Benefit Cards for Overseas Residents: No Fee Cards, Cashback Cards, "Lending" Cards

Note: All the KYC requirements below are "residents", not limited to nationality. That is, residents who can provide local residence proof, such as utility bills and credit card statements, will have different KYC difficulties depending on the requirements of different card issuers.

Coinbase Card: The Only "No Fee, No Loss" Payment U Card

As one of the largest and most compliant cryptocurrency exchanges in the world, Coinbase's debit card has significant advantages in user trust and fund security. This card is issued for users with Coinbase accounts, especially suitable for residents in the United States or the European Economic Area (EEA). Applicants must have a legal residency status and a real residence address in the location, and KYC verification is not supported for mainland China.

However, strict KYC brings high-end benefits: One of the main features of the Coinbase debit card is the exemption of all fees; its "native asset payment" mechanism allows users to directly use USDC and other stablecoins for daily consumption. The platform also supports transferring fiat money to USDC without fees, which greatly reduces the asset conversion costs for cardholders. Daily transactions and ATM withdrawals are usually free of fees, providing users with a near-lossless payment experience. In addition, the card is a VISA debit card, which can be used normally in merchants and services that support this network worldwide, covering a wide range of scenarios.

When users withdraw funds from Coinbase to their local bank account, if the account is located in a country or region supported by Coinbase, it can usually be credited quickly, and the entire process is widely evaluated as "smooth and stable". In addition, Coinbase occasionally launches cashback activities for debit card users, although the frequency is not high, it is an additional incentive for long-term cardholders.

In general, the Coinbase debit card, due to its compliance background, low fee system, and good fiat money deposit and withdrawal experience, has become one of the most popular crypto debit cards among users in Europe and the United States. For users who are already managing assets on the Coinbase platform, this card is undoubtedly an ideal extension of their on-chain assets in daily use scenarios.

Nexo Card: Cashback Credit Card for Residents in Europe

Nexo Card is launched by Nexo, a crypto exchange with headquarters in France and compliant licenses in the EU and UK, exclusively available to residents of the European Economic Area (EEA) and the UK. Chinese passport holders need European address proof and a residence permit to open an account. This card not only supports crypto asset consumption, but is also one of the few true "credit card model" U cards that allow users to pay first and repay later, and supports a relatively high cashback rate, making it one of the few sweet cards that can compete with North American credit cards.

Nexo Card belongs to the Mastercard network, and can be used in most merchants within the network.

The cashback mechanism of Nexo Card adopts a dynamic reward model based on user asset configuration. All daily consumption can get cryptocurrency cashback, basic cashback is 0.5% of the consumption amount, and the payment currency can be flexibly chosen as NEXO Token or Bitcoin (BTC) on the platform. When the total amount of crypto assets held in the user's account exceeds 5,000 USD, it will automatically be included in the Loyalty Program, and based on the proportion of NEXO tokens in the asset portfolio, it will be divided into different loyalty levels, thus obtaining higher cashback incentives.

Specifically, the highest platinum-level users can get up to 2% NEXO token cashback, or choose to return BTC at 0.5%; gold-level users are 1% and 0.3%; silver-level users are 0.7% and 0.2%; and the basic level remains at 0.5% NEXO or 0.1% BTC cashback. This tiered reward mechanism encourages users to hold more NEXO Tokens on the platform, thereby enhancing user stickiness and the intrinsic value support of the platform's token.

Regarding fees, Nexo Card has no annual or monthly fees, and the foreign exchange conversion fee structure is relatively transparent, but it is different from the traditional conversion fee design. If the transaction currency is the same as the card's default currency (euros or pounds), there is no charge ; for transactions where the card's currency (euros or pounds) is different from the merchant's local currency, the system will convert the transaction amount. If the transaction is settled in euros, Swiss francs, or pounds, the currency conversion fee is only 0.2% ; while for currencies in other countries or regions, it is 2% fee. In addition, all foreign currency transactions on weekends will also incur an additional 0.5% fee, which seems a bit strange.

Combined with its credit payment capability, dynamic cashback system, and crypto asset-oriented membership model, Nexo Card has established a relatively mature bridge between traditional financial systems and crypto asset usage scenarios, suitable for users residing in Europe who need cashback.

RedotPay (Red Card): Payment-Friendly Solution for Hong Kong, Macau, and Taiwan

RedotPay is a crypto payment company headquartered in Hong Kong, which officially launched its crypto payment card in late 2023, aiming to meet users' needs for using crypto assets in real-life scenarios. The core positioning of this card is similar to a traditional charge card (debit card), where users can have their crypto assets converted to fiat and used for consumption when they make purchases, without the need to pre-load funds into a fiat account or involve a credit loan. Unlike previously mentioned exchange-backed card products, RedotPay is not a virtual currency exchange, but focuses on providing blockchain-based payment solutions, so its card products are more focused on the usage paths of on-chain assets themselves.

This card currently does not support registration and use by residents of mainland China, but can be applied for and used in multiple overseas regions. The overall fee structure is moderate, the comprehensive fee is approximately 1% to 3%, depending on the currency conversion and consumption scenario. A major highlight of the RedotPay card is its direct support for Binance Pay, allowing users to complete recharge and settlement through the Binance wallet system, giving it a certain advantage in interoperability within the on-chain ecosystem.

In terms of card types, RedotPay provides a VISA card, which is relatively rare in the crypto card market. In addition, the card is free of annual fees, reducing the long-term card-holding costs for users, but the application of a physical card requires a one-time fee of 100 USD.

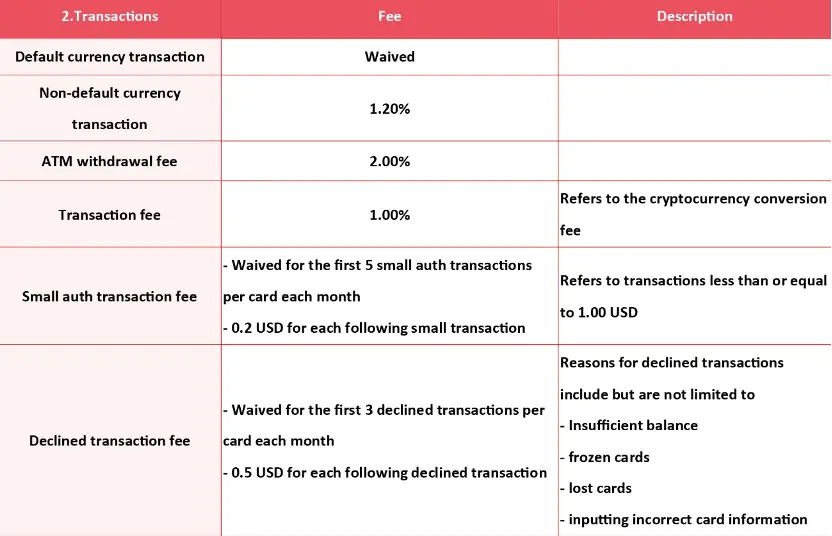

In terms of fees, Redotpay provides a complete fee table:

It can be seen that the transaction fee for non-default underlying currency is 1.2%, the ATM withdrawal fee is 2%, and the transaction fee is 1%. These fees do not include fees charged by platforms such as Alipay.

Overall, the RedotPay crypto card targets overseas users with cross-border living or online consumption needs, suitable for those who want to directly use on-chain assets for daily payments and do not rely on centralized exchanges for asset custody. It is one of the few products in the crypto card market that takes a "light platform" approach.

Decentralized Project U Card Series, Focused on Self-Managed Funds

MetaMask Card: Low-Fee Payment Card Launched by MetaMask

MetaMask Card is a lightweight cryptocurrency payment tool launched by the crypto wallet giant MetaMask, primarily targeting existing wallet users, aiming to extend on-chain funds directly to daily consumption scenarios. This card is currently in the early open phase, only open for registration in certain countries and regions, including the United States (excluding New York and Vermont), the United Kingdom, EU member states, Switzerland, Mexico, Colombia, and Brazil.Its global version has not been fully opened yet.

Metamask card also belongs to the Mastercard merchant network. It is reported that there will be a physical metal card as airdrop benefit in the future.

Regarding asset support, the MetaMask Card currently supports USDC, USDT, and wETH three tokens, all funds must be stored in Linea network, users need to cross-chain their related assets to this chain for recharge. After recharging, the card can be directly connected to Apple Pay or Google Pay to realize mobile payments, without needing a physical card. During the usage process, the system will convert the selected cryptocurrency to fiat currency in real-time for each transaction and settle it in the local currency, with the conversion process completed instantly when the transaction is initiated.

Regarding fees, using stablecoins such as USDC or USDT for payment, only one Linea network gas fee is required, usually around $0.02; while for non-stablecoins such as wETH, an additional 0.875% on-chain swap fee is also required. All fees will be displayed in the card's backend "Manage" module after the transaction is completed, and users can view detailed bills, including exchange rates, deduction amounts, and fees.

Additionally, MetaMask Card provides 1% USDC cashback for all consumption, further enhancing the cost-effectiveness of using on-chain assets directly in consumption scenarios. This cashback model and visualized fee structure make this card very suitable for users familiar with DeFi and on-chain operations, especially those who have already used the MetaMask wallet as their primary asset management tool.

1inch Card: The Magical "Lending" Card That Allows Borrowing Stablecoins for Consumption

Launched by the crypto aggregation trading platform 1inch, the 1inch Card is supported by Crypto Life and uses Baanx as the compliance deposit and withdrawal service provider. This card not only has conventional on-chain payment capabilities , but also provides users with more strategic asset consumption options through the "mortgage + lending" model. In terms of identity verification, the KYC procedure required for the 1inch Card is similar to other products in the Baanx ecosystem, mainly open to compliant residents of the European Economic Area and the UK, requiring local address proof.

Unlike most crypto cards that directly consume on-chain assets, 1inch Card allows users to mortgage BTC or ETH to borrow stablecoins for daily consumption. Users can choose USDC, USDT, or EURT as the borrowed currency, and set the loan period between 6, 12, 18, or 24 months. This lending model is particularly favorable for users who are long-term bullish on crypto assets. For example, when the price of Bitcoin is low, users can mortgage BTC to borrow stablecoins for consumption, without directly consuming their own Bitcoin. When Bitcoin prices rise, users can choose to repay the stablecoins, thus redeeming higher-value original assets. This mechanism not only preserves the potential for asset appreciation but also meets the need for real liquidity.

Certainly, stablecoin lending inevitably involves interest, but as long as the increase in the collateral asset can cover this interest, the advantages of the lending card are very obvious. According to the official website, during the loan period, interest must be automatically repaid monthly, and the deduction operation is automatically completed through the system's stablecoin wallet. Once the loan and interest are fully repaid, users will get back all their collateral assets as they were originally.

At the same time, the platform supports users to obtain a credit limit of up to 60% of their collateral asset value.

Regarding the payment currency, 1inch Card supports mainstream Layer 1 assets such as BTC, ETH, LTC, and XRP, but does not currently support Layer 2 network assets. When users make purchases, the system will automatically convert it to fiat and complete the settlement. The platform's fee structure is relatively complex but clear: the card's consumption fee is 2%, the exchange between cryptocurrencies and the conversion from crypto to fiat is 1.75%; if it is a crypto asset withdrawal, the fee is 0.4% to 0.5%; and if it is a bank transfer to withdraw fiat, the fee is 3.49%. In terms of card services, there is no annual fee or maintenance fee, but the withdrawal of British pounds incurs a fee of €2.50, and the withdrawal of foreign currency incurs a fee of €3.00 plus 1.5%.

The above fees seem high, but in fact, they are not cumulative. That is, direct card swipe consumption is 2% plus potential foreign exchange conversion fees, and after converting to fiat at a rate of 1.75%, it can be directly consumed in fiat, overall, it is not much different from other crypto assets.

Additionally, 1inch Card provides 2% crypto cashback per transaction, further improving the cost-effectiveness of daily use. Combined with its stablecoin lending capability based on collateral, flexible term setting, and wide range of supported asset types, 1inch Card is not just a consumption card, but also a mini financial toolkit for crypto asset holders, occupying a unique position in the increasingly integrated DeFi and real-world financial scenarios.

Disclaimer: Contains third-party opinions, does not constitute financial advice

AI Practical Guide

This column focuses on the real progress of Agents: technological evolution, application implementat

Crypto Weekly

Tracking on-chain movements of the smart money and institutions

Frontier Insights

Spotlight on Frontier, trending projects, and breaking events

Blowup Alert

As the 2026 crypto bear market deepens, exit scams and project blowups are becoming increasingly fre

Regulatory Watch

American Crypto Act – timely interpretations of policies worldwide

Popular Airdrop Tutorial

Selected potential airdrop opportunities to gain big with small investments

FusnChain

FusnChain